Finance talk focuses on dual-class structure

UTAR Centre for Accounting, Banking, and Finance (CABF) and the Department of Finance at the Faculty of Business and Finance (FBF) organised a webinar titled “Dynamics of Borrowing Costs: Evidence from Dual-Class Firms” on 7 July 2021 via Microsoft Teams.

Dr Nurul (left) thanking Prof Yu for conducting the talk

The talk was presented by a distinguished speaker, Prof Dr Yu Min-Teh, who is a lifetime Chair Professor at Providence University and Chiao Tung University. Prof Yu has published more than 60 papers at SSCI and SCI journals in areas of financial risk management, banking, and insurance. Some of his research papers have been published in the Journal of Banking and Finance, Journal of Risk and Insurance, Journal of Banking and Finance, Journal of Risk and Insurance, Journal of Financial Service Research, Journal Real Estate Economics and Finance, and Journal of Business Finance and Accounting. Also present at the webinar were CABF Chairperson Dr Nurul Afidah Mohamad Yusof, lecturers and students from FBF.

Prof Yu elaborating on the dual-class structure

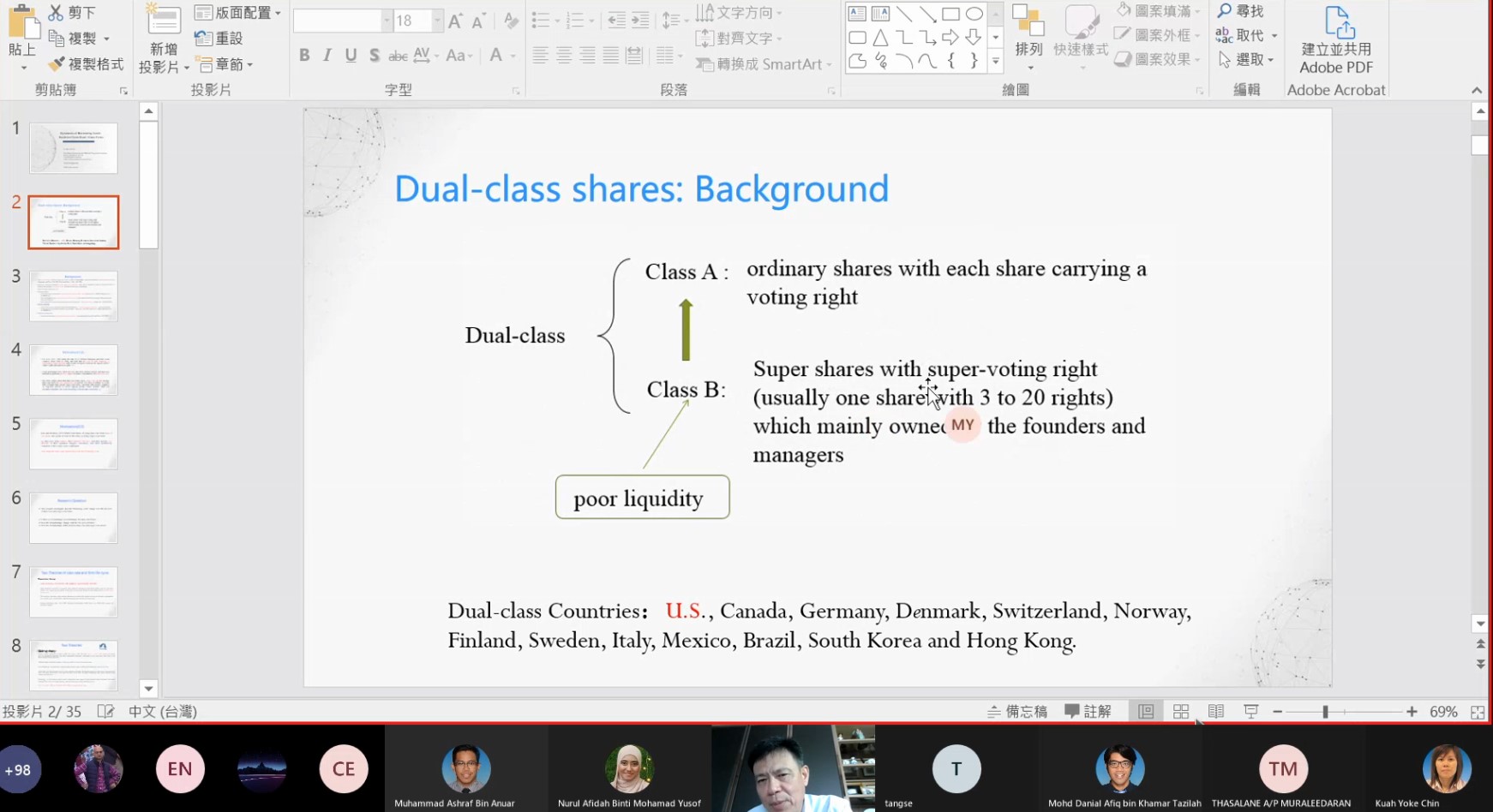

Prof Yu started his talk by introducing dual-class shares (DCS). He said, “DCS arises when a company issues two classes of shares. The class of shares offered to the public usually have limited or no voting rights, while the class issued to founders have more voting rights. In a dual-class structure, voting rights and cash flow rights are decoupled and this structure is used by founders and executives to achieve control of a firm in excess of their equity ownership.”

“Some of the countries that allow dual-class shares are the U.S., Canada, Germany, Denmark, Switzerland and Hong Kong. Approximately seven per cent of the U.S. firms issue dual class shares. Additionally, many technology firms, such as Alibaba and Apple prefer a dual-class share structure as it allows the founders and executives to maintain control through higher voting rights. However, according to studies, the optimal firm share structure in terms of shareholder wealth maximisation is one share one vote,” he added.

In terms of market valuation, Prof Yu highlighted that dual-class stocks were typically valued less than similar single-class stocks. He explained, “However, in the hands of competent management, the long term value of dual-class shares has the potential to increase. Such an upward trend is also prevalent with high growth firms. On the other hand, dual-class firms tend to face agency issues as the excess control rights with the founders may be detrimental to minority shareholders. Dual-class firms also have higher information asymmetry than single-class firms.”

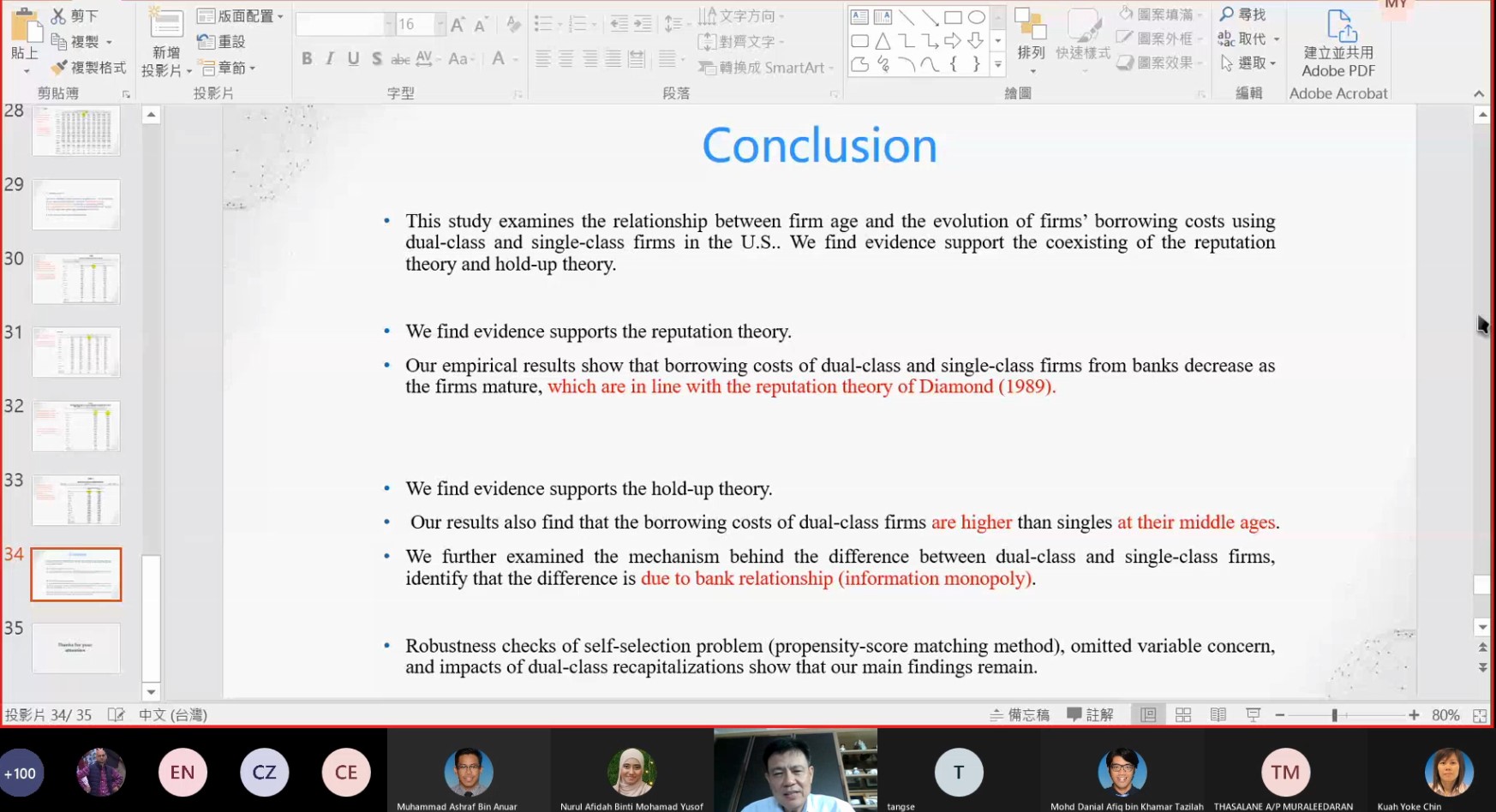

Further on, he introduced one of his ongoing studies which examines the borrowing costs of dual-class and single-class firms and how such costs change over the lifecycle of the firms. He examined whether there was a cost advantage for dual-class firms and how the advantages differ between dual-class and single-class firms. Prof Yu identified the Reputation Theory and Hold-Up Theory to examine loan rates and firm life cycle. He explained, “The Reputation Theory states that a firm’s borrowing costs decrease as the firm increases in reputation/age. The resulting reputation effect encourages borrowers to choose safe projects to safeguard their reputation, in order to reduce borrowing costs. The Hold-up Theory implies that as banks gain an information monopoly over their borrowers, the banks extract rents from these firms in the form of higher borrowing rates. This theory implies a lifecycle profile for a firm’s borrowing costs. In this sense, firms are held up by the banks due to lack of competition among the banks.”

Prof Yu sharing his research findings

Prof Yu concluded the interesting talk with findings from his study of U.S. dual-class firms. He said, “Results show evidence supporting the co-existence of the reputation theory and hold-up theory. For Reputation Theory, the borrowing costs of dual-class and single-class firms from banks decrease as the firms mature. For Hold-up Theory, the evidence shows that the borrowing costs of the dual-class firms are higher than singles at their mid-life cycles and that the difference is due to bank relationships and information monopoly.

The talk ended with a Q&A session.

![]()

© 2021 UNIVERSITI TUNKU ABDUL RAHMAN DU012(A).

Wholly owned by UTAR Education Foundation (200201010564(578227-M)) LEGAL STATEMENT TERM OF USAGE PRIVACY NOTICE