The Department of Banking and Risk Management organised an online talk titled Intelligent Banking: Model-Driven Decisions & Real-Time Finance on 10 December 2025 via the Microsoft Teams platform. The session was delivered by Mr Teoh Kah Ming, Head of Enterprise Risk Management at Alliance Bank Malaysia Berhad. The one-hour talk attracted 291 participants, comprising UTAR staff and students.

The talk aimed to demystify the concept of “intelligent banking” by moving beyond the buzzwords of Artificial Intelligence (AI) to highlight how banks practically apply data analytics, predictive modelling and human expertise to manage one of their most critical functions—risk management.

Mr Teoh began the session by addressing the conflicting perceptions often associated with banking: on one hand, rigid and traditional practices, and on the other, futuristic, opaque AI-driven systems. He explained that the reality lies in a careful balance, where technology enhances and empowers human expertise rather than replacing it.

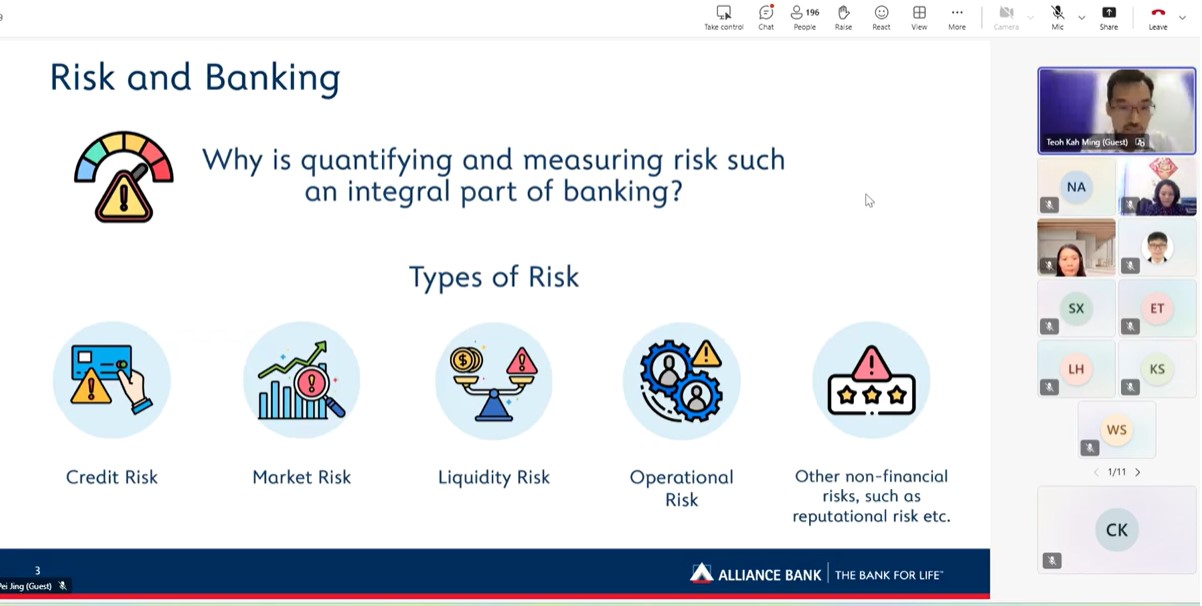

He further emphasised a fundamental principle that distinguishes banking from many other industries: risk is the product. Unlike most businesses that treat risk as an undesirable by-product, banks regard risk as a core feature of their business model. Mr Teoh elaborated on two primary types of risk—credit risk, which refers to the possibility of borrowers defaulting on repayments, and liquidity risk, which involves the challenge of borrowing short-term from depositors while lending long-term for assets such as 30-year mortgages. He highlighted that effectively managing this mismatch is where banks create value, and failures in this area could threaten a bank’s survival.

A significant portion of the talk was devoted to the concept of sampling bias, illustrated through a well-known World War II analogy. Mr Teoh recounted how Allied engineers initially proposed reinforcing returning aircraft at the areas showing the most bullet damage. However, a statistician identified a critical oversight: the analysis only included planes that survived. Aircraft hit in vital areas, such as engines, never returned and were therefore excluded from the data.

Drawing parallels to banking, Mr Teoh explained that this “survivorship bias” poses a major challenge in credit risk modelling. Banks often rely solely on data from approved loans—the “planes that returned”—while lacking information on rejected applicants. To address this issue, he introduced the concept of reject inferencing, a statistical technique used to estimate the behaviour of rejected applicants to reduce bias in risk models.

The speaker also highlighted the importance of human judgement in model-driven decision-making, noting that “every model is wrong, but some are useful.” Given that risk is the core product of banking, he cautioned against over-reliance on automated models. Banks therefore institutionalise human overrides, allowing credit experts to challenge model recommendations. He added that frequent overrides, occurring in half of all cases, serve as an early warning signal that the model itself may be flawed and requires recalibration.

Mr Teoh further addressed the misconception that success in AI stems from sophisticated algorithms alone. Instead, he stressed that effective data management—often perceived as “unexciting”—is the true foundation of success. He shared that up to 80 per cent of a modeller’s time is spent cleaning, preparing and validating data, underscoring the necessity of strong domain knowledge alongside technical skills.

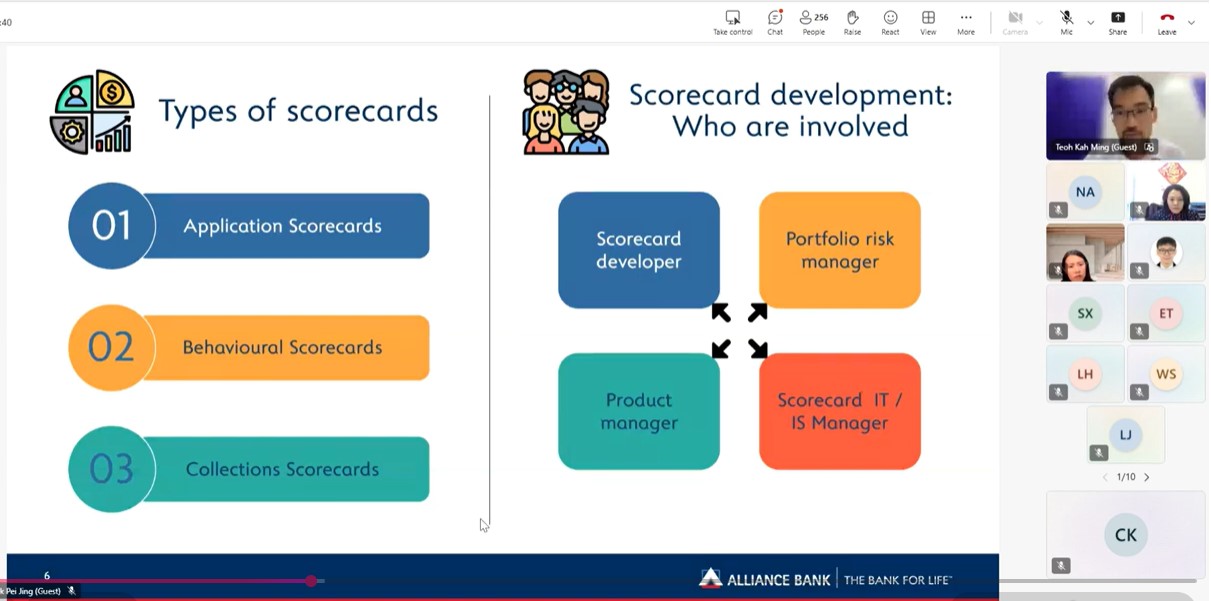

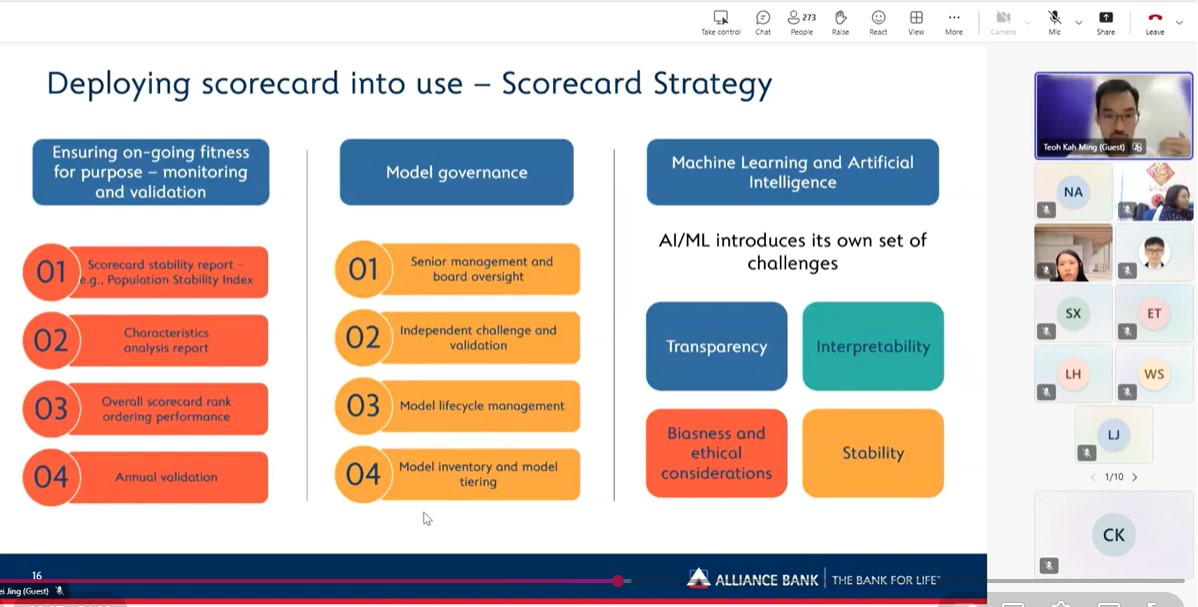

The talk also covered key risk management tools, particularly credit scorecards. Mr Teoh outlined three main types: application scorecards for new loan assessments, behavioural scorecards for existing customers, and collection scorecards for managing delinquent accounts. He compared modern machine learning approaches with traditional logistic regression, noting that while machine learning models are powerful, traditional methods are often preferred for their transparency and ease of regulatory compliance.

In conclusion, the webinar reinforced that intelligent banking is not about removing humans from decision-making processes. Instead, it involves a synergistic system where machine-driven analysis and expert human oversight complement and balance each other.

The session concluded with an interactive question-and-answer segment, during which Mr Teoh addressed questions on fairness in AI. He emphasised that achieving fairness requires actively identifying and managing historical biases embedded within training data, rather than merely excluding sensitive variables such as race or gender.

The speaker, Mr Teoh started the talk by addressing the conflicting images people often have of banking

Mr Teoh explaining the risks of the banking industry

Mr Teoh explaining the scorecards

Mr Teoh answering questions from the audience during Q&A

© 2025 UNIVERSITI TUNKU ABDUL RAHMAN DU012(A).

Wholly owned by UTAR Education Foundation (200201010564(578227-M)) LEGAL STATEMENT TERM OF USAGE PRIVACY NOTICE